Client Relationship & Service

6 MIN ARTICLE

For advisor use only. Not for use with investors.

What’s an ideal client, anyway? The answer differs from practice to practice. But if you haven’t defined yours, you may be wasting valuable time and energy.

KEY TAKEAWAYS

- Defining your ideal client is an essential strategy for analyzing and segmenting your client roster.

- Segmenting your book of business into groups can help you streamline services and increase efficiency.

- Apply the real relationship value (RRV) formula for segmenting clients and prioritizing your service model.

Have you defined the ideal client for your business?

If you’ve never thought about it before, your initial description of “ideal” might be something like: high net worth, doesn’t complain, asks very little. Although this describes someone who might be easy to deal with, that doesn’t necessarily make this person the ideal client for your business. It doesn’t even mean you are the right advisor for this client.

With a more intentional approach, you might define an ideal client as someone whose needs, wants and concerns align with your competencies. It’s someone able and willing to pay for advice, who will value and follow your guidance and with whom you would enjoy building a rapport and possibly a friendship.

The process of defining your ideal client is less about hypothetical perfection than about identifying a set of business-boosting characteristics among the investors you serve. This client segmentation process can, in turn, shape how you serve different cohorts, what you charge them for these services and how much time you allocate to servicing them.

Why segment clients?

Client segmentation is a strategy widely used by many sales organizations. However, it’s typically underutilized among advisors — in particular, new advisors or those with less-established advisory practices, who tend to cast a wide net and take on any prospect in an effort to build business.

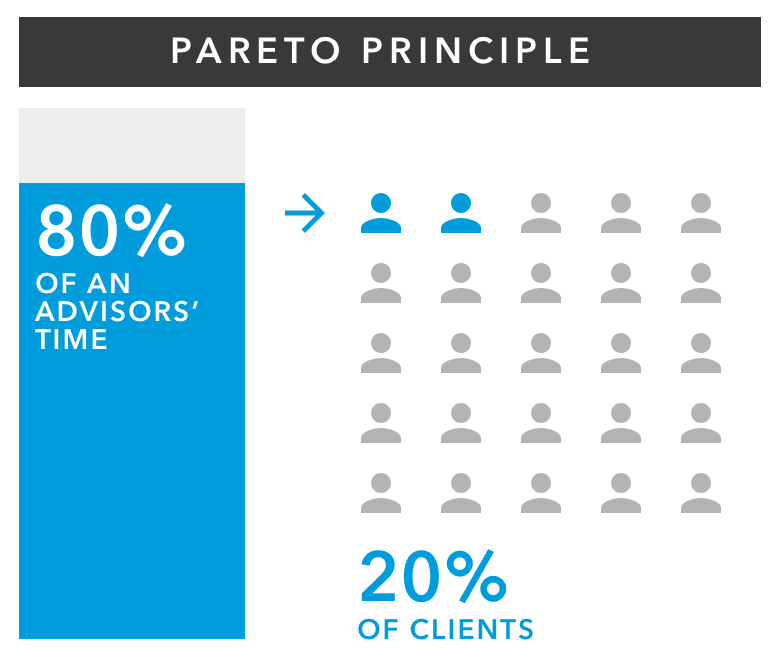

But even those who are new to the profession could use segmentation to nurture and grow a client base. Why? Think of the Pareto Principle or “80/20 rule.” You’ll likely spend 80% of your time and energy with about 20% of your clients. So, you want to be sure it’s the right 20% — those who lead to increased revenue and more referrals.

Segmenting your book of business into groups can help you streamline services for each type of client, freeing up the time to work more efficiently with all clients and enhance your offering to higher-value ones

Make the grades

To segment your book, you’ll need to assign each client a grade. The grades can be as simple as A, B and C (although nobody should get an F in this world), divided according to your preferred metrics. Some advisors use assets under management as the only clear guideline. In reality, the score you assign should incorporate multiple factors. Some may be more subjective, such as future earnings potential, a shared philosophy that leads to an easy working relationship or the ability to make quality referrals.

The grades you assign will help you prioritize how much time to spend with different types of clients. You may also want to upgrade clients who have high potential. For example, if someone has only invested $100,000 with you but has discretionary income of $150,000, you might still assign that client a B or even an A based on the relationship’s potential. Similarly, you may consider how much a “B” client is contributing to a retirement plan and, anticipating you may one day be in a position to receive a rollover, service them like an A client.

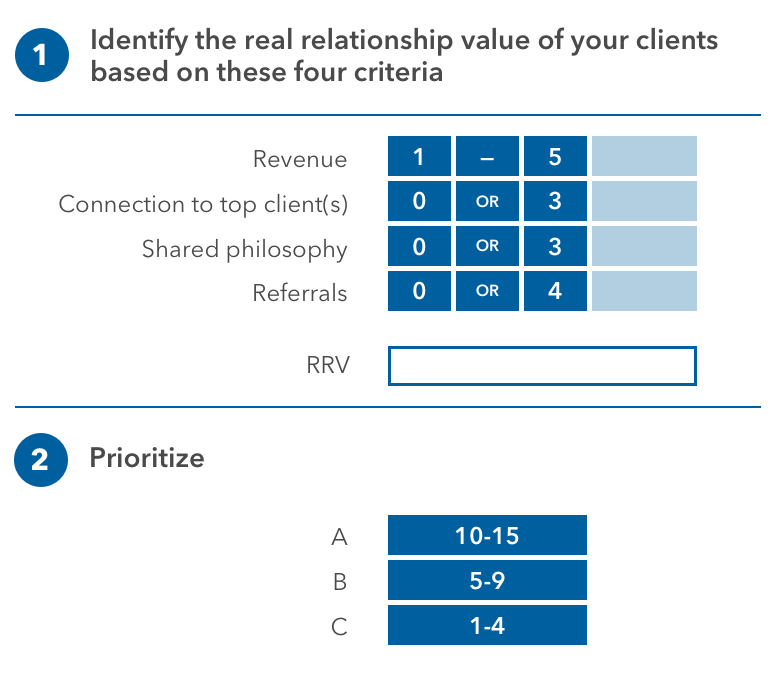

Identifying B clients with A-list potential is a qualitative call, but it doesn’t require a crystal ball. Using a point system to assess different criteria can help you determine the real relationship value. You can develop your own model or utilize our simple approach (below).

Real relationship value: A formula for success

When segmenting your client book, you can determine how to prioritize what you value most. Use this tool to get a sense of the real relationship value of each client.

Source: Capital Group

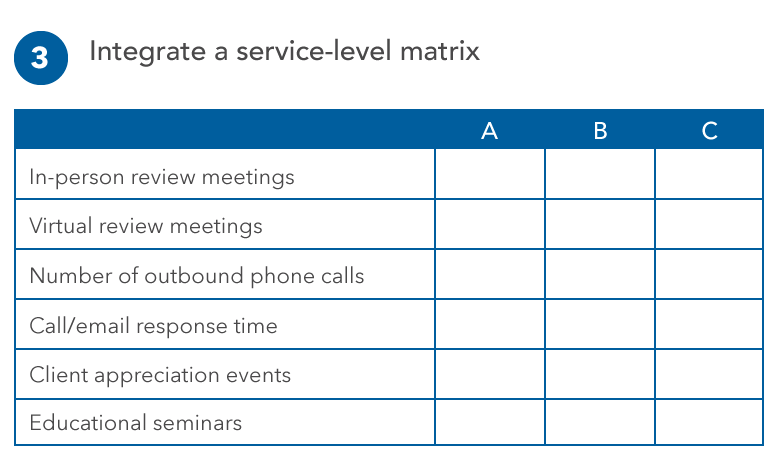

The ABC service model

The next step is to tailor the service you provide to each segment.

A-list clients will get the most white-glove touchpoints, which can include monthly mailings or emails, quarterly or semiannual statements, in-person or videoconference meetings at least twice a year, plus ad hoc phone calls, personal notes or chance meetings. You may decide to have a client event once or twice a year, dedicated solely to A clients.

B-list clients may receive nearly as many touchpoints as A clients, but require less time commitment. They live in a sort of “sweet spot” for the client and your business. Communications may include a monthly newsletter and quarterly statements, perhaps with a personal note. B-list clients would also get two meetings a year and an invite to one client event or educational seminar.

C-list clients may get an automated monthly email from you in addition to an in-person annual review. When these clients call because of market volatility, you should call them back. But here’s a situation where segmentation comes into play. During periods of market volatility, you may get an influx of calls that you need to return. Segments can be used by your administrative staff to help prioritize the order in which you do so.

Map your model

Use the table below to define your segment-based service and communication strategy.

Source: Capital Group

Find your ideal client balance

In terms of client mix, it may seem like a book full of A-list clients would be ideal. But the math won’t work. Remember that 80/20 rule? You’ll inevitably be spending most of your time with a small segment of your overall clientele and need to make sure it’s the right segment. In other words, you simply won’t have enough time to service a book of nothing but A clients.

In general, your clientele should be composed of 25% A clients, and keep C-list clients to a maximum of 15%. That means the majority of your clients will be Bs, so it’s important to get their service model right.

And it’s not just about proportions. Overall numbers matter too. As a new or popular advisor, the temptation may be to amass a lengthy client list. But can you really service 250 households? Moreover, if they each invest only $50,000, that’s a lot of stress in return for limited compensation.

In the end, building a roster of clients aligned to your competencies and objectives — then applying a service model that supports them effectively and efficiently — is a great recipe for strengthening your practice.

Related content

-

Client Conversations

-

Client Relationship & Service